The problem with insurance is you only talk to your customers when they have a problem; it’s hard to generate a positive moment in the relationship. Insurers are dropping billions of dollars to get more involved in consumer health and wellness, in an attempt to shift their relationship with customers from “payer” to “partner” or even “carer.”

Competition for this relationship is intense. Insure-techs and e-tailers are introducing new business models and capabilities daily. Apple is expected to launch Health Insurance in 2024, leveraging its customer relationships and health data. [1] Insurers need to act now to deepen customer relationships, and expand their role beyond financial health, to include healthy living and social engagement. AXA Group’s entry into telemedicine and health services paints a compelling story of how to deepen relationships with customers.

AXA’s CEO Thomas Buberl described the company’s ambition “to go beyond insurance to become a true partner to our customers.” AXA wanted to be a first point of contact for their customers for primary healthcare, to integrate different building blocks of the care path, and to simplify and better manage care in the service of the patient.

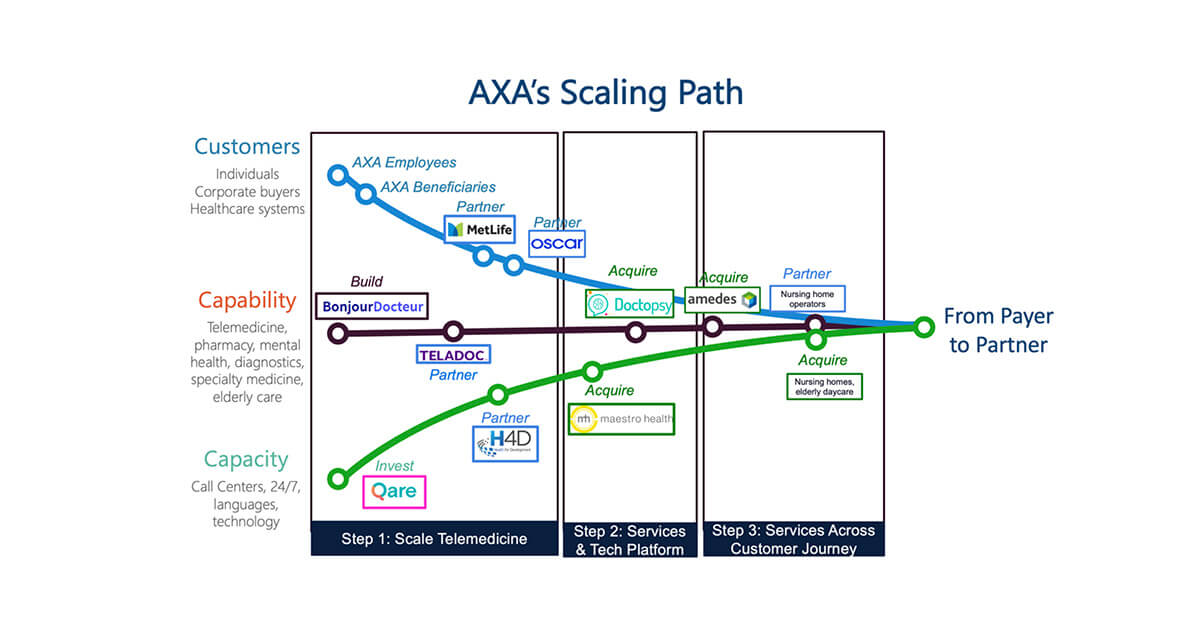

Scaling Path

In 2014, AXA entered the healthcare market by building France’s first teleconsultation service, BonjourDocteur, which allowed AXA employees to make virtual appointments with doctors, download prescriptions, find a local pharmacy, and manage their own medical profile. The program was so successful, AXA extended the service to beneficiaries in 2015. They continued to scale telehealth, adding 5X new providers through a partnership with Qare, a virtual network of French general practitioners and specialists serving corporate subscribers. This expansion gave AXA the ability to offer 24/7 access to a network of experienced, internationally qualified doctors in more than 20 languages. A partnership with Teladoc (2018) added doctors in 8 new regions, and AXA’s acquisition of Doctopsy (2020) broadened their services to include mental health services over the phone.

AXA continued to expand its capacity to serve customers through a partnership with H4D. H4D offers a self-contained medical kiosk called the Consult Station that enables patients to take their own vital signs, conduct self-checkups using video tutorials, and get medical teleconsultations via BonjourDocteur. This partnership extended AXA’s customer reach to new rural populations in towns that suffer from a lack of doctors.

Over the past two years, AXA’s Virtual Doctor Service went from being used in 76 countries to 141 countries, and utilization increased from 26% of registered users to 64% of users. [2]

Scaling Opportunity that Didn’t Work

One scaling opportunity where AXA stumbled was Employee Assistance Programs (EAPs). They acquired Maestro Health and its promising all-benefits platform maestroEDGE™ for $155 million in 2018, and sold it in 2022 for $22 million to AI-tech firm Marpai. What happened?

The ambitions of AXA and Maestro health were aligned. As the deal closed, Maestro Health Founder, Rob Butler blogged, “the 42nd most recognizable brand in the world shares the same vision, strategy, culture and aspirations as we do – to ultimately transform the U.S. healthcare market by simplifying the experience, lowering costs and empowering consumers.” [3] Maestro added 500 groups and 1 million lives to AXA’s customer base, brought a technology platform to support AXA’s continuum of care ambition, and provided a solid footprint in the US market.

However, AXA’s strategy was to operate Maestro as a stand-alone subsidiary, maintaining its own identity, mission and team. Maybe it was this hands-off strategy that didn’t work. After all, between 70 and 90 percent of acquisitions fail. [4] Holding a venture too far from the core prevents the core business from capturing the synergies of the combined entity. It also prevents the venture from leveraging the customers, capabilities and capacity of the core.

Or maybe AXA had too many irons in the fire. At the same time as the Maestro Health acquisition, AXA was investing in a broad set of opportunities including Apricity (virtual fertility), birdie (elderly home care), and Padoa (occupational health). There is no evidence that AXA was able to scale ventures in these areas.

What’s Next for AXA’s Payer-to-Partner Strategy

AXA will need to stay aligned on its ambition, focus innovation efforts, and continue to pivot with learning. While their investment in EAPs didn’t pan out, their success in telemedicine and their quick move to divest or pivot from what wasn’t working is encouraging. Andy O’Cain, Global Head of Distribution, AXA Global Healthcare, hints that they have plenty of other digital tools and guidance coming soon. [1] It’s also likely that disruptive opportunities will be identified by AXA Next, the company’s new-ventures arm, established in 2019 with €200m in annual funding.

AXA’s Investment Managers Alts group (Alternative Investments),is also involved in scaling the company’s health ventures, and is strategically creating even more opportunities to position AXA as “partner” or “carer.” In 2021, the group acquired Amedes, a provider of medical diagnostics services in Germany, Belgium and Austria, giving them access to 75+ laboratories and specialty medicine sites, offering services ranging from fertility medicine, to rheumatology, to oncology. [5] They are also making significant investments investing in a portfolio of senior housing in the UK, Germany, Finland, France, Ireland. [6] They continued to expand in 2022, entering the Spanish healthcare market to develop a 270-bed nursing home and mental health clinic, with a separate on-site elderly daycare, and making a significant investment in the Japanese market. [7] [8]

What’s Next for Incumbents

As AXA’s CEO Thomas Buberl prescribed, incumbents must “go beyond insurance to become a true partner to customers.” Telehealth proved to be an effective entry point for AXA, enabling AXA to become the first point of contact and orchestrator of the customer’s healthcare journey. They alleviated the pain of accessing and orchestrating care, and solidified their position as a real partner to their customers, not just a payer. They used a combination of build-buy-partner to assemble and scale the capabilities, customers, and capacity needed to serve their beneficiaries across the globe.

Incumbents can learn from the example set by AXA. Generate more positive moments in your relationship with customers. Ask 3 questions:

- What is your ambition for deepening customer relationships?

- How can you develop new ventures that create different touchpoints with customers?

- How might you scale a new venture by combining assets you have, can build, or acquire?

[av_hr class=’default’ icon_select=’yes’ icon=’ue808′ font=’entypo-fontello’ position=’center’ shadow=’no-shadow’ height=’50’ custom_border=’av-border-thin’ custom_width=’50px’ custom_margin_top=’30px’ custom_margin_bottom=’30px’ custom_border_color=” custom_icon_color=” id=” custom_class=” template_class=” av_uid=’av-l36asn’ sc_version=’1.0′ admin_preview_bg=”]